The global stablecoin market has grown into the hundreds of billions of dollars, while governments and financial regulators are developing new rules to oversee their use in payments and commerce. Reports from the Bank for International Settlements (BIS), the International Monetary Fund (IMF), and the Financial Stability Board (FSB) show that stablecoins are increasingly being considered as part of the broader digital payments landscape rather than remaining limited to cryptocurrency trading.

This shift has sparked comparisons between conventional banking systems and emerging regulated stablecoin networks. As these technologies evolve, individuals and businesses are beginning to consider how they may influence everyday transactions and financial planning, particularly when sending money internationally or managing digital assets.

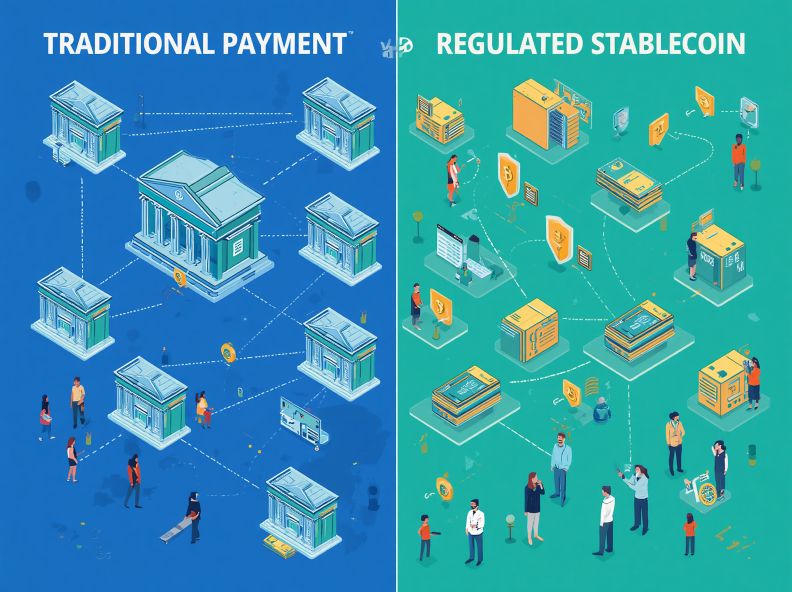

Traditional Payment Systems: Familiar but Often Slower

Traditional banking infrastructure has long provided consumers with reliable payment services backed by established regulations and deposit protections. Banks operate within comprehensive legal frameworks that support fraud prevention, dispute resolution, and anti-money laundering requirements.

However, international transfers often involve several financial institutions before reaching the recipient. Research from the World Bank indicates that cross-border remittances can still carry relatively high fees and settlement delays, especially when payments move across multiple jurisdictions. While many countries have introduced faster domestic payment systems, international transfers remain more complex.

Regulated Stablecoins: Faster Settlement with New Possibilities

Stablecoins are digital tokens designed to maintain a stable value, usually by being backed by reserves linked to national currencies. When issued under regulatory oversight, they may allow transactions to settle much faster than some conventional cross-border payment methods.

Experts from the Bank for International Settlements note that programmable digital assets and blockchain technology could improve payment efficiency by reducing intermediaries involved in settlement. Industry initiatives by regulated financial institutions are exploring ways to integrate stablecoins into existing payment networks rather than replacing banks entirely.

Lower transaction costs could particularly benefit migrant workers, international businesses, and online commerce where frequent cross-border payments are common.

The Other Side of the Debate

Despite these potential advantages, regulated stablecoins also raise important policy questions. Reports from the Financial Stability Board emphasize that strong reserve management, operational resilience, and transparent governance are essential to protect users.

Consumer advocates likewise point to the importance of clear redemption rights, cybersecurity safeguards, and effective supervision. Without consistent international standards, differences between national regulations could create uncertainty for users and service providers operating across borders.

The International Monetary Fund has also highlighted that large-scale adoption could influence monetary policy and financial stability if regulatory frameworks fail to keep pace with technological innovation.

Finding a Practical Balance

Rather than viewing banks and stablecoins as direct competitors, many policymakers see opportunities for coexistence. Traditional financial institutions continue to provide trusted customer relationships, lending services, and regulatory compliance, while digital payment infrastructure may improve transaction speed and operational efficiency.

Several central banks and regulators are therefore focusing on rules that encourage innovation while maintaining safeguards for consumers and financial markets.

Conclusion

The future of payments will likely combine established banking services with carefully regulated digital technologies. Stablecoins may offer faster settlements and more efficient international transfers, yet their long-term success will depend on strong oversight, transparent reserve practices, and public confidence.

As payment systems continue to evolve, individuals may benefit from periodically reviewing their broader financial priorities, budgeting approaches, and digital asset exposure. Understanding how new payment technologies fit within personal money management can help consumers make informed decisions as financial services continue adapting to a more connected global economy.